The Six-Month Window Opens April 16: Four Moves to Make Between Now and October 15

Tax season is wrapping up. In a few days, your CPA will be somewhere between relieved and exhausted. You’ll click “submit” (or “extend”), and then you’ll move on.

Back to the OR. Back to the schedule. Back to the rhythm that defines most of your year.

And that instinct to move on? That’s exactly the problem.

Because the six months between April 15 and October 15 are often when some of the most valuable financial moves of the year can be made. Or missed. The difference between those two outcomes comes down to whether you have a protocol for the window, or whether you just let it close.

The Window Most Surgeons Waste

Consider a surgeon earning $820K through an S‑Corp, who files an extension every year and doesn’t think about taxes again until October. That’s not unusual. It’s the norm for many high‑income practice owners with demanding schedules.

But here’s what often happens in that gap. Six months pass. The S‑Corp salary stays where it was last year. The retirement plan stays the same. The entity structure stays the same. And by the time October rolls around, every meaningful optimization window has either narrowed or effectively closed for that tax year.

The cost of inaction during this period is real. In a typical high‑income practice with the right plan design, it’s common to see potential optimization opportunities in the range of tens of thousands of dollars per year; in many coordinated cases, $35,000 to $60,000 of first‑year benefit is not unusual, though actual results vary. Compounded over a decade, that kind of gap can become a six‑figure difference in long‑term wealth, especially when tax‑advantaged savings have more years to grow.

The surgeons who capture that value aren’t doing anything exotic. They’re following a protocol, the same way you’d follow a post‑operative rehab timeline. Sequenced, time‑bound, and grounded in the principle that early action compounds better than late reaction.

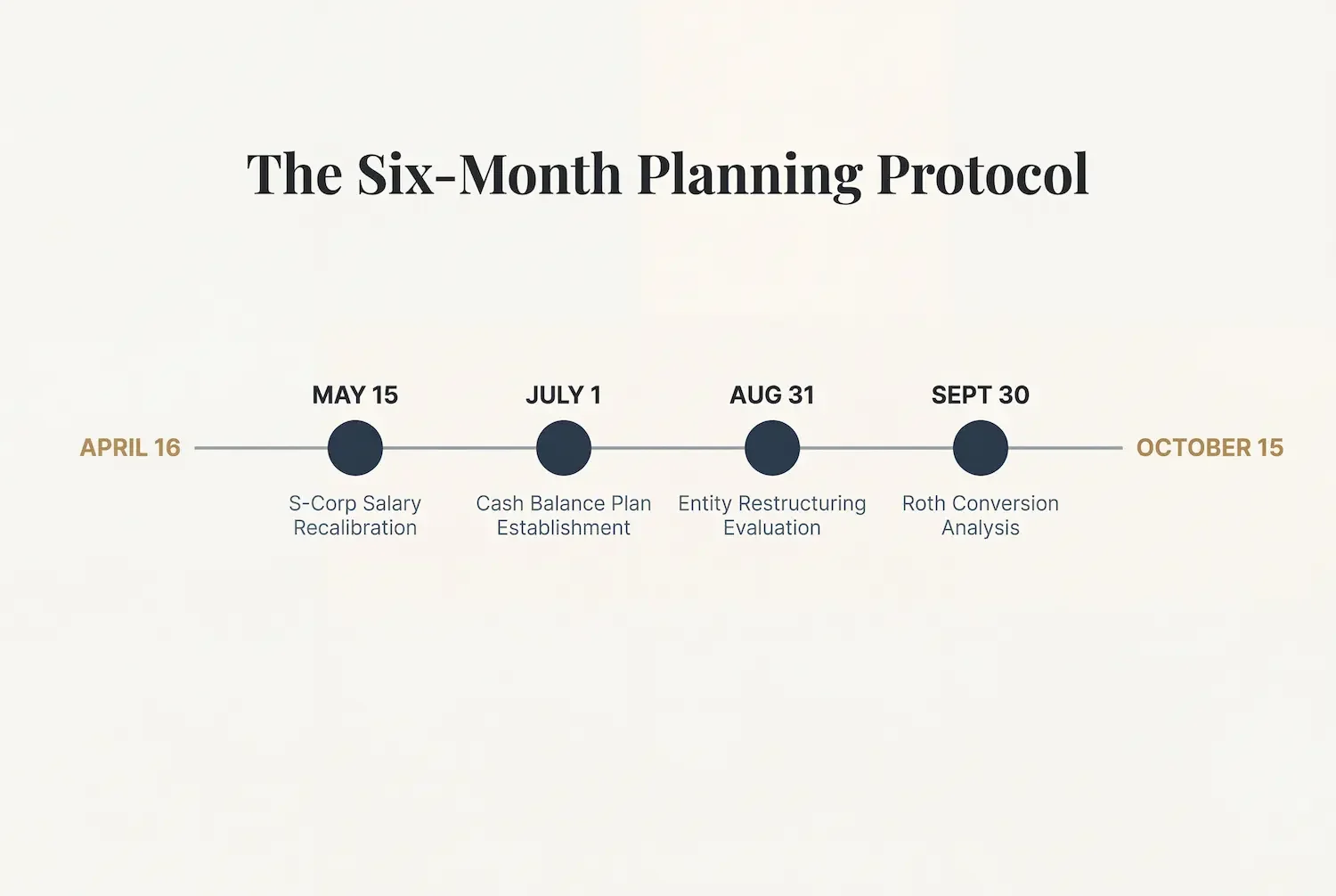

The Four‑Move Protocol

Here are four specific moves that are often best initiated during the April‑to‑October window, each with a practical timeline that matters. These are illustrations, not one‑size‑fits‑all recommendations.

Move 1: S‑Corp Salary Recalibration (Target: May 15)

Your S‑Corp reasonable compensation was probably set when your practice looked different than it does today. Revenue has changed. Reimbursement has changed. Your retirement plan structure may have changed. But the salary? That number tends to stay frozen in time.

Recalibrating your S‑Corp salary in the first half of the year gives your payroll provider time to adjust withholding and gives your retirement plan administrator time to update contribution calculations. Waiting until Q4 compresses both.

Here’s an illustrative example of the math that can make this worth prioritizing. A surgeon currently paying herself $300,000 through the S‑Corp, who recalibrates to $350,000 in a way that remains consistent with IRS “reasonable compensation” expectations, may unlock an additional ~$20,000 or more in annual employer retirement plan contributions, depending on the 401(k)/profit‑sharing and cash balance design and current IRS limits. The incremental payroll tax cost on the extra $50,000 of wages—primarily Medicare taxes once you are above the Social Security wage base—is typically several thousand dollars per year in combined employer and employee FICA, still resulting in a net increase in tax‑deferred savings for many surgeons.

The key is that any salary change must be documented and defensible under reasonable‑compensation rules, not just engineered to maximize plan contributions. A target date around May 15 gives you enough runway to coordinate with your CPA, run a compensation analysis if needed, and implement cleanly for the balance of the year.

Move 2: Cash Balance Plan Establishment (Target: July 1)

If you’re over 50, earning $700K or more, and you don’t have a cash balance plan, this is often one of the highest‑leverage structural additions available to you—when it fits your risk tolerance, cash‑flow, and staffing profile.

A cash balance plan is a type of defined benefit plan that can, in many designs, support six‑figure annual tax‑deferred contributions—often in the $150,000 to $350,000 range for older, high‑income owners—on top of 401(k) contributions, subject to IRS section 415 limits, actuarial calculations, and nondiscrimination testing. Those contributions grow tax‑deferred and are deductible to the practice, but they also come with funding obligations and administrative complexity that need to be modeled carefully.

There’s also a timing reality. Establishing a new qualified cash balance plan requires plan design, plan document preparation, actuarial certification, and compliance setup, which typically takes 6 to 10 weeks from engagement to completion in a real‑world setting. Starting in April or May often gives you a July 1 effective date and allows meaningful funding for the current year. Waiting until September or October frequently makes it impractical to design, adopt, and fund a new plan for that tax year, even though some plans can technically be adopted by the tax return due date (including extensions) under current law.

Think of July 1 as a practical implementation target for meaningful first‑year funding, not a statutory IRS deadline. Every month of delay reduces the flexibility you and your actuary have to design and fund the plan in line with your goals.

Move 3: Entity Restructuring Evaluation (Target: August 31)

If your practice structure hasn’t been reviewed in three or more years, the April‑to‑October window is often the right time to evaluate whether your current entity setup still serves your financial, risk, and transition goals.

Common triggers for restructuring: you’ve added a partner or associate, your revenue has shifted meaningfully, you’re considering an ASC ownership stake, or you’re within five years of a potential practice transition. Any of these changes may warrant a shift from a single‑entity S‑Corp to a multi‑entity structure, or vice versa, and may raise questions about how personal goodwill, real estate, or ancillary income streams are structured.

Entity restructuring takes time. Legal documents need drafting. Tax elections need filing. Operating agreements need updating. For many structures, you want everything in place as of January 1 to have a clean year for accounting and tax purposes, even though specific IRS election deadlines can vary by entity type and may allow for late elections with relief. An August 31 start date is a practical latest point to begin this work if you want a coordinated legal and tax implementation by year‑end, with your attorney and CPA both at the table.

Move 4: Roth Conversion Analysis (Target: September 30)

With the One Big Beautiful Bill (OBBBA) extending the current individual income tax bracket structure, including the 37% top rate, beyond 2025 under current law, the Roth conversion calculus has shifted. The question for many high‑income surgeons is less “should I ever do a Roth conversion?” and more “at what marginal rate, in which years, and in what amounts might conversions make sense relative to my retirement and estate plans?”

The answer depends on your full‑year income picture, which starts to clarify in Q2 and Q3. Running the conversion analysis in the summer, when you have enough year‑to‑date data to model but enough time to execute, lets you identify specific conversion amounts that target your projected retirement tax bracket, consider your state‑tax trajectory, and integrate with your estate planning goals and any OBBBA‑related changes (like SALT and deduction rules).

Practically, many surgeons benefit from running this analysis by late September, so there’s time to adjust estimated taxes and execute conversions before the December 31 deadline for that tax year. Waiting until November or December often means you are forced to “ballpark” income numbers instead of modeling them carefully, and you have less flexibility to adjust if circumstances change.

The Protocol in Practice

Here’s what this can look like for a surgeon who files an extension on April 15 and commits to a structured protocol. The following is a hypothetical example for illustration only; your results will differ.

By May 15, the S‑Corp salary has been recalibrated from $300,000 to $350,000 based on a documented reasonable‑compensation analysis. The payroll adjustment is in place and retirement plan contributions are being calculated against the new W‑2.

By July 1, a cash balance plan has been established with a half‑year funding target of $100,000, consistent with IRS limits and actuarial recommendations. The plan document is executed and the first contribution is scheduled according to the funding timeline.

By August 31, an entity‑level restructuring evaluation has been completed. The review identifies an opportunity to separate personal goodwill or ancillary revenue into a distinct entity in preparation for a potential practice transition in three to five years, coordinated by the surgeon’s attorney and CPA. Legal documents are in progress for a January 1 effective date for the new structure.

By September 30, a Roth conversion analysis identifies, for example, a $40,000 conversion opportunity in a quarter where income was lower than projected due to a surgical conference and vacation schedule, at a targeted marginal rate the surgeon and CPA are comfortable with.

In a case like this, the combined first‑year value of these four moves might reasonably fall in the $35,000 to $60,000 range in tax‑advantaged savings and structural improvements, depending on plan design, state taxes, and the surgeon’s broader balance sheet. If the same surgeon had waited until October or later, the cash balance plan opportunity for that tax year would likely have been lost and the Roth conversion analysis would have been constrained by timing and incomplete data.

The practical value of starting early is not a guaranteed dollar amount, but an increase in the opportunity to capture materially more tax‑efficient savings and better‑aligned structures than would be possible in a last‑minute scramble.

The Underlying Principle

In surgery, the preparation before the procedure determines the outcome more than the procedure itself. Pre‑operative planning, imaging review, patient positioning, instrument selection: all of that happens before the first incision. And it’s what often separates a good outcome from a great one.

Your financial life works the same way. The six months of preparation between April 15 and year‑end often determine whether December is a scramble or a celebration. Whether you’re reacting to deadlines or executing a plan you built six months earlier.

The surgeons who build wealth most efficiently aren’t necessarily the ones with the highest collections. They’re the ones who treat the planning window with the same discipline they bring to the OR.

April 15 is next week. The window opens the day after. The question is whether you’ll walk through it with a protocol, or let it close with a promise to “get to it next year.”

Capably Yours,

Jared

Disclaimer

This article is for informational and educational purposes only and does not constitute investment, tax, or legal advice. It does not take into account the specific objectives, financial situation, or needs of any particular person. You should consult your own tax, legal, and investment professionals before acting on any information contained herein. Capable Wealth, a New York registered investment adviser, provides advisory services only where properly licensed or exempt from licensing.