The 5-Year Exit Timeline: What to Start Doing Now If You Want Options Later

If a patient came to you with a degenerative condition, you wouldn't wait until they couldn't walk to start treatment. You'd assess the imaging, establish a baseline, and build a multi‑year management plan. You'd sequence the interventions. You'd give yourself time.

Your practice exit deserves the same approach.

Most surgeons start thinking about practice transition somewhere around 12 to 18 months before they want to leave. By that point, the timeline is already compressed. There's less room to restructure the entity, document personal goodwill, recruit an associate, or position the practice for competitive bids. The result? A sale that happens on someone else's terms, at a price driven more by urgency than by strategy.

Now that April 15 is behind you and conference season is in full swing, practice transition is likely showing up in every other hallway conversation. PE firms are hosting dinners. Colleagues are comparing deal terms. And the question "have you thought about what's next?" is getting harder to deflect.

Good. Let it land. But before you respond to it, let's build the protocol.

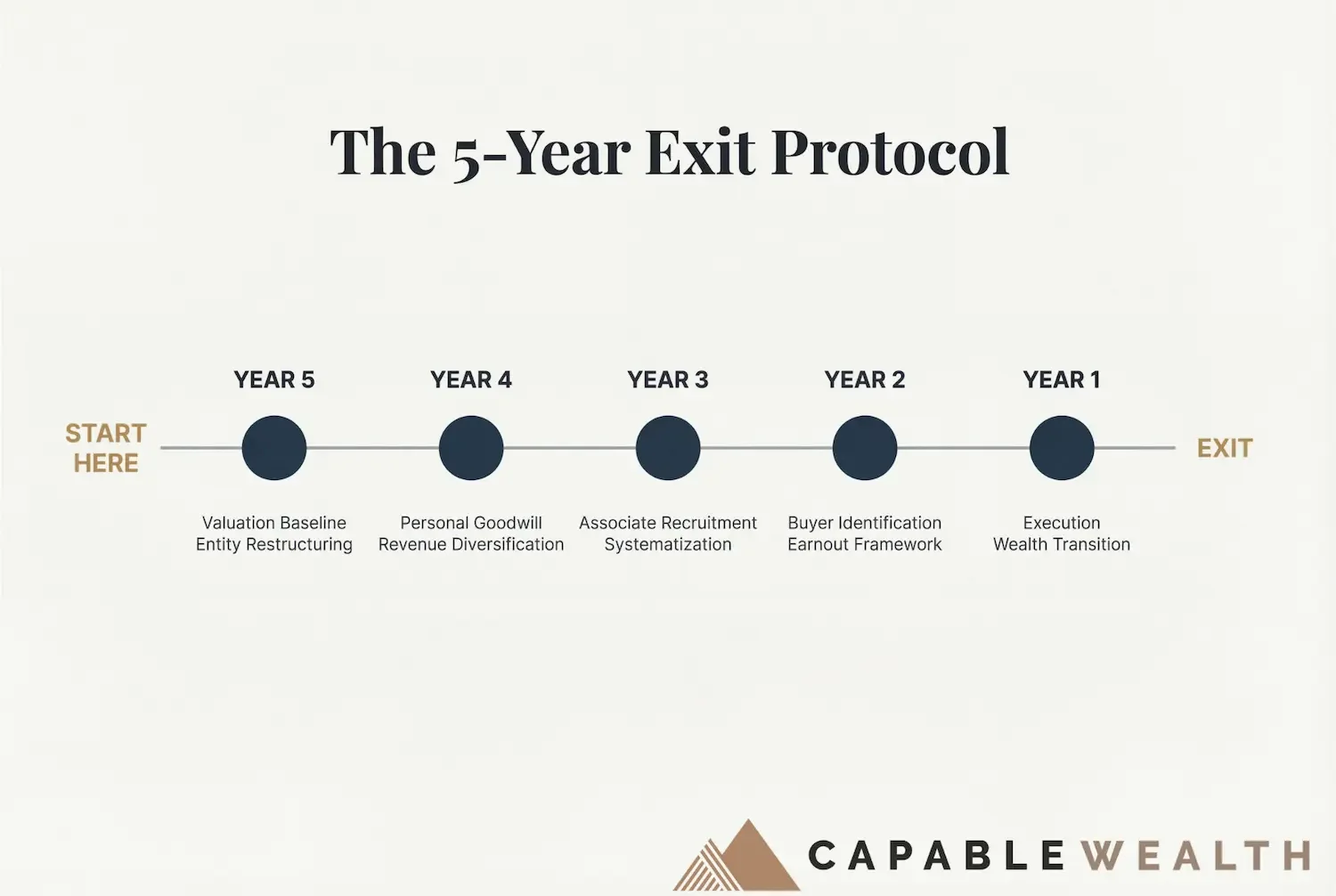

Why Five Years (and Not Two)

The difference between a 5‑year exit timeline and a 2‑year timeline comes down to one word: options.

With two years, you largely take what's available. The entity structure is whatever it is. The valuation reflects the practice as it stands. The buyer pool is whoever's currently interested. And the negotiating leverage often tilts toward the buyer, because you've signaled that you're ready to leave.

With five years, you can deliberately shape the outcome. You evaluate and, if appropriate, restructure the entity while there's no transaction pressure. You document personal goodwill when it can be established credibly (rather than asserted retroactively during negotiations). You diversify revenue to support a higher valuation. You bring in an associate to demonstrate that the practice can operate without you. And when buyers come to the table, you have the most powerful thing a seller can have: the ability to walk away.

Let's walk through what each year might look like.

Year 5: Valuation Baseline and Entity Restructuring

This is the diagnostic year. Before you can build a treatment plan, you need imaging.

Start with a practice valuation. Not the back‑of‑the‑envelope number you carry in your head, but a formal assessment of the practice's enterprise value, your personal goodwill, and the gap between them. This baseline becomes the benchmark against which every future decision is measured.

At the same time, evaluate your entity structure. If you're operating as a single‑entity S‑Corp (or similar structure) and you're five years from a potential transition, this is the moment to explore—with your attorney and tax advisor—whether separating personal goodwill into a distinct agreement, establishing a management company, or restructuring ownership makes sense. From a tax and regulatory perspective, structures that have been in place for years rather than months are generally more credible when scrutinized in connection with a sale, especially where goodwill allocations are involved.

Consider a surgeon at age 55, with a practice currently valued at $2.8 million based on existing operations. In Year 5, a formal valuation reveals that the enterprise value is $2.8 million, but $1.1 million of that is attributable to the surgeon's personal goodwill (reputation, referral relationships, patient loyalty). In many medical practice sales, properly structured and substantiated personal goodwill may be eligible for long‑term capital gains treatment under current law, depending on your specific facts and existing agreements. Documenting it years in advance, rather than a few months before closing, generally makes the position more credible if it is later examined by the IRS or a buyer’s advisors.

Personal goodwill is a contested and highly fact‑specific area; whether and how it applies in your situation is ultimately a legal and tax determination.

Year 4: Personal Goodwill Documentation and Revenue Diversification

Year 4 is about building value that the practice can carry forward after you leave.

Personal goodwill documentation can accelerate here. This may include non‑compete or restrictive covenant agreements, referral source analysis, patient retention data, and evidence that a meaningful portion of the practice's revenue is tied to your individual reputation and relationships, as opposed to just the entity. The goal isn't to inflate value artificially. The goal is to capture, on paper, the value that already exists in your professional identity but would otherwise be invisible or under‑recognized in a transaction.

Revenue diversification also begins in Year 4. If 100% of your practice revenue comes from surgical procedures you personally perform, the practice's transferable value is limited. Buyers typically pay higher multiples for diversified revenue: ancillary services, ASC ownership stakes, non‑surgical revenue streams, and referral networks that generate value beyond any single provider.

In our illustrative scenario, the surgeon adds a 20% ownership stake in an ambulatory surgery center and builds a structured referral network with three primary care practices. These additions increase practice enterprise value from $2.8 million to $3.4 million by Year 3 in the hypothetical, because they represent revenue that doesn't walk out the door when the surgeon does. This is an example, not a prediction; actual results vary by market, payer mix, and execution.

Year 3: Associate Recruitment and Systematization

This is the year that most directly impacts valuation, because it addresses the question every buyer asks: "Can this practice survive without the founder?"

If the answer is no, the multiple drops. If the answer is yes, the multiple rises. For smaller physician practices, the difference in valuations between surgeon‑dependent and systematized practices can be meaningful: for illustrative purposes, a move from a 3x to a 4x multiple on $700,000 in normalized EBITDA changes the valuation from $2.1 million to $2.8 million on that metric alone. Actual multiples vary widely by specialty, scale, growth profile, and buyer type.

Recruiting an associate in Year 3 gives you two full years to integrate them, transfer patient relationships, and demonstrate that the practice can produce consistent revenue with a second provider. It also reduces your personal clinical load, which can be reinvested into transition planning, relationship building with potential buyers, or simply into the quality of your remaining working years.

Systematization goes hand in hand with this. Documented workflows, codified clinical protocols, standardized patient communication, structured staff roles, and clear governance all make the practice more transferable and less personality‑dependent.

Year 2: Buyer Identification and Earnout Framework

By Year 2, the practice is positioned. The entity has been evaluated and, if appropriate, restructured. Personal goodwill is documented. Revenue is diversified. An associate is integrated. Now it's time to understand the buyer landscape.

Buyer identification in Year 2 (not Year 1) gives you time to evaluate options without pressure. The landscape may include private equity platforms, hospital systems, individual physician buyers, and management services organizations. Each comes with a different deal structure, a different earnout framework, and a different post‑sale reality for the selling surgeon.

The earnout deserves particular attention. In many PE‑backed transactions, a portion of the purchase price is contingent on post‑sale performance. Understanding the earnout structure (how long, based on what metrics, what happens if targets aren't met) is often worth more than focusing only on the headline multiple. A $4.2 million deal with a 40% earnout tied to three years of revenue targets is a fundamentally different transaction than a $3.8 million deal with 100% cash at close.

Year 2 is when you develop your negotiating framework: what you'll accept, what you won't, and what your walk‑away number looks like. Having this framework before any buyer makes an offer is the difference between negotiating from strength and reacting from hope.

Year 1: Execution, Closing, and Wealth Transition

Year 1 is execution. The treatment plan has been built. The imaging has been reviewed. The positioning is complete. Now you operate.

The closing itself, while significant, is the smallest part of the process in terms of strategic impact. The value was primarily created in Years 5 through 2. Year 1 is about executing cleanly: finalizing deal terms, managing the tax consequences of the sale, and transitioning the proceeds into a wealth structure that serves your next chapter.

Tax planning at the point of sale is critical and ideally has been in motion since Year 5. For high‑income surgeons, the gap between federal ordinary income rates and long‑term capital gains rates (plus applicable surtaxes) can translate into several hundred thousand dollars of tax difference on a multi‑million‑dollar sale, depending on filing status, state of residence, and overall income. In an illustrative $4.2 million scenario, that difference could easily exceed $600,000 in combined federal and state taxes, but the actual figure is highly situation‑dependent.

Personal goodwill allocation, installment sale structuring, charitable planning through donor‑advised funds, and state tax residency decisions can all factor into the ultimate tax outcome. While some decisions can be made late in the process, many of the most impactful strategies require years of lead time and coordination among your CPA, attorney, and advisor.

The Math That Makes This Real (Hypothetical Illustration)

Here's how the 5‑year approach changes the outcome for our illustrative surgeon.

Starting position at age 55: a practice valued at $2.8 million under current operations.

With a 5‑year timeline in this hypothetical: Year 5 restructuring separates personal goodwill conceptually and adds $200,000 in documented enterprise value. Year 4 revenue diversification (ASC stake, referral network) increases practice value from $2.8 million to $3.4 million. Year 3 associate recruitment reduces surgeon‑dependence, supporting a higher multiple—illustratively from 3x to 4x—and a practice valuation of $4.2 million based on $700,000 of normalized EBITDA. Year 2 buyer identification in a competitive market yields several offers. Year 1 execution closes at $4.2 million with a structure designed to improve tax efficiency relative to the starting point, subject to applicable tax rules and professional advice.

Without the timeline: the same surgeon at 60, ready to leave, sells the practice in its current state for $2.8 million. No personal goodwill analysis or documentation. No entity restructuring. No competitive buyer process. The sale happens on a compressed timeline, with limited negotiating leverage and fewer planning options to improve the tax outcome.

The difference in gross valuation in this example is $1.4 million. Same surgeon. Same basic practice. Same market. The only variable is when the planning started.

In the hypothetical, starting five years earlier instead of two might also support roughly $300,000 to $500,000 in additional tax savings through better allocation and capital‑gains‑oriented planning, although real‑world results will vary and are not guaranteed. Combining the higher enterprise value (about $1.4 million above the baseline) with those potential tax savings suggests that the total financial impact of starting five years early instead of two could be well north of $1.7 million in this scenario. This is a simplified illustration, not a projection.

The Surgeons Who Exit Well

The surgeons who get the best outcomes in practice transitions share something in common. They didn't get lucky with timing or stumble into a generous buyer. They started early enough to have choices.

Conference season is a useful time to start thinking about what's next. You'll hear pitches. You'll compare notes with colleagues. You'll sit through presentations about “partnership opportunities” and “liquidity events.” All of that is valuable input.

Just make sure you're processing it through your own timeline, not someone else's. A PE firm buying dinner has their timeline. Your colleague who just closed a deal had their timeline. The surgeon sitting across the table at the conference has theirs.

Yours starts with one question: if you want options in five years, what do you need to start doing now?

The answer, as with any complex case, is a protocol. Sequenced. Time‑bound. Built on a baseline assessment and refined as new information emerges.

You've been building treatment plans your entire career. This one just happens to be for you.

Capably Yours,

Jared

Disclaimer

This article is for informational and educational purposes only and does not constitute investment, tax, or legal advice. It does not take into account the specific objectives, financial situation, or needs of any particular person. You should consult your own tax, legal, and investment professionals before acting on any information contained herein. Capable Wealth, a New York registered investment adviser, provides advisory services only where properly licensed or exempt from licensing.